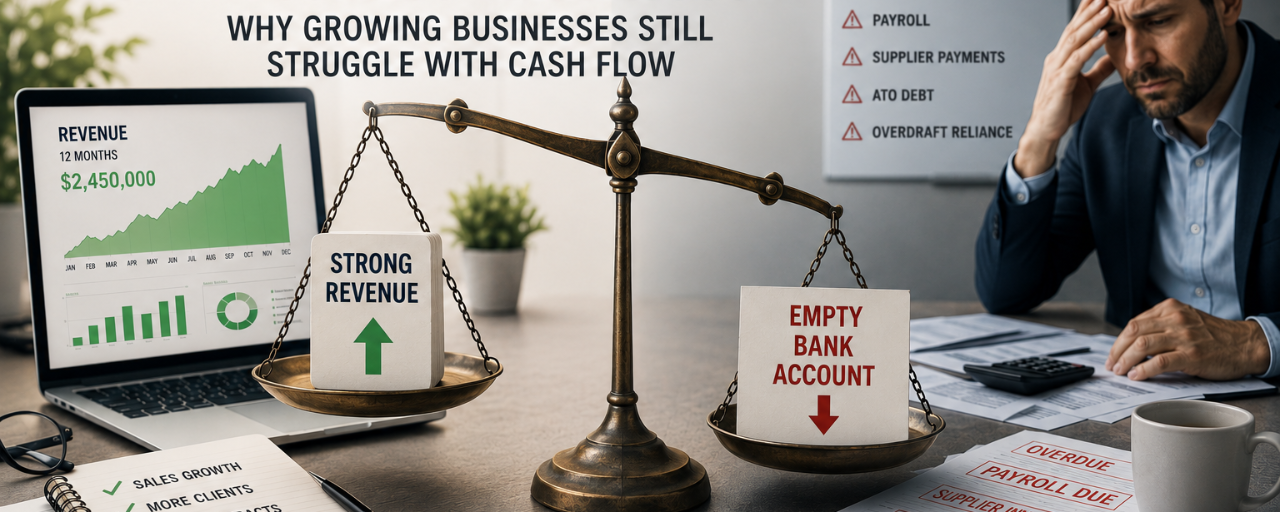

For many Australian business owners, strong revenue often creates the impression that a business is financially healthy. Sales may be increasing, invoices are being issued consistently, and overall growth can appear stable on paper, but despite this activity, many businesses still experience ongoing pressure in their bank accounts. This creates confusion and stress, particularly when the business appears profitable yet continues to struggle with day-to-day financial obligations. This is one of the most common challenges faced by SMEs, where a business looks successful externally but is actually experiencing significant cash flow strain and, in some cases, moving toward financial distress.

The fundamental issue is that revenue and cash flow are not the same thing. Revenue represents the total sales a business generates within a specific period, but it does not reflect whether the cash from those sales has actually been received. A business can show strong turnover while still being unable to meet essential obligations such as wages, supplier payments, rent, and tax commitments. This becomes especially problematic when customers take 30, 60, or even 90 days to settle invoices, as the business must continue funding its operations long before the actual cash arrives.

Many business owners only recognise the seriousness of this issue when financial pressure begins to affect day-to-day operations. This may appear as difficulty meeting payroll obligations, delays in paying suppliers, increasing ATO debt, or growing reliance on credit facilities to bridge short-term gaps. While financial reports may still show profitability, the lack of available cash creates ongoing operational strain that can quickly escalate if it is not addressed early.

Growth Can Quietly Create Cash Flow Pressure

Business growth is often seen as a positive milestone, but it can also create significant cash flow pressure if not managed carefully. As revenue increases, businesses typically need to expand operations by hiring additional staff, purchasing more stock, investing in systems, or increasing marketing activity. These costs are generally incurred upfront, while customer payments are received later, which creates a timing mismatch between outgoing expenses and incoming cash.

When a business secures multiple large contracts or experiences rapid expansion, this pressure can intensify, particularly in industries where payment cycles are long or projects require significant upfront investment. Although the business may appear successful from the outside, the internal cash position can become increasingly strained. Without proper cash flow management, growth can place a business under financial stress rather than improving stability.

Late Payments Are a Silent Business Risk

Late payments from customers remain one of the most persistent causes of cash flow problems in Australian businesses. Many business owners spend a significant amount of time chasing overdue invoices while still trying to manage daily operations, which creates additional pressure on already stretched resources. To manage the resulting shortfalls, businesses often rely on overdrafts, credit cards, short-term lending, or delayed tax payments in order to maintain operations.

While these measures may provide temporary relief, they do not resolve the underlying issue and can gradually create a cycle of dependency on external funding. Over time, this reactive approach can reduce financial stability and increase stress within the business, particularly when overdue payments continue to accumulate and cash flow remains inconsistent.

Revenue Without Profitability Is a Hidden Risk

A common misconception in business is that increasing revenue automatically leads to financial stability, but this is not always the case. A business may generate high turnover while still operating on very thin margins, particularly when costs such as labour, materials, freight, and finance repayments continue to rise. In some situations, higher sales can actually increase financial pressure if each transaction contributes only a small amount of profit or requires significant upfront expenditure.

Smaller businesses with strong margins and consistent cash flow are often in a stronger financial position than larger businesses that rely heavily on volume without sufficient profitability. This highlights the importance of focusing not only on sales growth but also on how much cash the business retains after all expenses have been paid.

Early Warning Signs of Cash Flow Stress

Cash flow problems typically develop gradually rather than appearing suddenly, and they are often preceded by a series of warning signs that indicate increasing financial pressure within the business. These signs may include consistently low bank balances despite strong sales, delays in paying suppliers, increasing ATO or BAS debt, reliance on overdrafts or credit cards, and difficulty meeting payroll obligations. In many cases, business owners also experience ongoing financial stress or find themselves making short-term decisions that prioritise immediate survival over long-term stability.

When these warning signs begin to appear, they should not be ignored, as they often indicate underlying cash flow issues that will continue to worsen without intervention. Early recognition of these indicators can make a significant difference in preventing further financial deterioration.

When Cash Flow Becomes an Insolvency Risk

Cash flow issues become more serious when a business is no longer able to pay its debts as they fall due, which is a key indicator of insolvency under Australian law. At this stage, financial pressure may escalate to the point where directors are exposed to legal and financial risks associated with trading while insolvent.

Warning signs of potential insolvency risk may include mounting ATO debt, unpaid superannuation obligations, increasing creditor pressure, reliance on borrowing to cover essential operating costs, and difficulty meeting payroll without external assistance. When these issues are present, it is important to seek professional advice early, as delaying action can significantly reduce available options and increase overall risk.

Why Cash Flow Management Matters More Than Revenue

Improving cash flow is not always about increasing sales but rather about improving how efficiently money flows through the business. Simple operational improvements such as issuing invoices promptly, implementing automated payment reminders, offering easier digital payment options, and monitoring overdue accounts more closely can have a significant impact on cash flow stability. Faster payment cycles reduce reliance on external funding and help create a more predictable financial position, which supports long-term resilience.

By focusing on cash flow efficiency rather than revenue alone, businesses can improve financial stability without necessarily needing to increase sales volume. This approach allows for better planning, reduced financial stress, and stronger control over day-to-day operations.

What To Do If Your Business Is Under Pressure

When a business begins experiencing ongoing financial pressure, it is important to take action early rather than waiting for the situation to worsen. Early intervention may involve reviewing cash flow structure, assessing profitability, negotiating with creditors, or exploring restructuring options depending on the severity of the situation. Taking proactive steps at an early stage can help preserve business value and reduce financial and legal exposure.

Delaying action often reduces available options and increases the likelihood of more serious outcomes, particularly if debts continue to accumulate and cash flow remains constrained.

How Insolvency Options Can Help

At Insolvency Options, we work with Australian business owners who are experiencing financial pressure to help them understand their position and explore available pathways forward. Whether a business is dealing with early-stage cash flow concerns or more serious insolvency risks, seeking timely professional advice can make a significant difference in achieving a more controlled and informed outcome for directors, stakeholders, and the business itself.